Table of Content

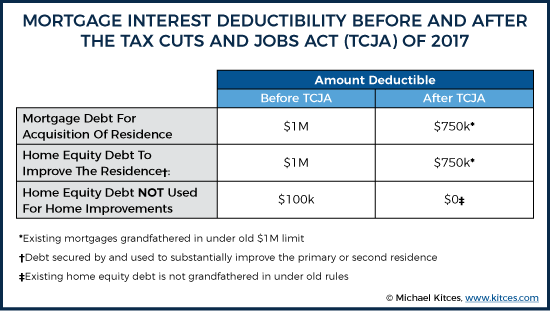

Under prior law, you could also deduct the interest on up to another $100,000 of debt if the loan proceeds were used to buy or improve a first or second residence (or another $50,000 if you used married-filing-separately status). The additional amount could be in the form of a bigger first mortgage or a home equity loan. Either way, it was characterized for tax purposes as home equity debt. If you own a home and are planning to claim the home equity loan interest deduction, there are a few things to remember. For example, you cannot take the deduction if you are using home equity proceeds to pay for personal expenditures or consolidate credit card debt. The same goes if you are taking out a loan and letting the money sit in the bank as your just-in-case fund for emergencies.

Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories. Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range can also impact how and where products appear on this site. While we strive to provide a wide range offers, Bankrate does not include information about every financial or credit product or service. This is the last year youll be able to take the residential energy credit.

How We Make Money

Highest rate is applicable to taxable income above $500,000 for single taxpayers and head of household, and $600,000 for married taxpayers filing jointly. So, many taxpayers tapped into their home equity to pay for, say, vacations, college tuition, vehicle purchases and living expenses. And they counted on deducting interest on those loans each tax year. The new rules for deducting interest on home equity loans will put a wrench in those plans, starting in 2018. The good news is not all these changes will apply this upcoming year. On December 2017, President Donald Trump signed the new tax reform law called Tax Cuts and Jobs Act.

A personal exemption is a sum of money you can deduct for yourself and any dependents from your taxable income. A family of four, for example, would have received $16,200 in exemptions last year. Here’s a look at the deductions you won’t be able to claim on your 2018 taxes ― and what you can do instead. Unless you’re in the military, moving expenses you pay out of pocket for a job relocation are no longer deductible.

Is There A Best Time Of Day For Therapy? Here's What Therapists Say.

If you use married-filing-separately status, the limit is halved to $375,000. Thanks to grandfather provisions for pre-TCJA mortgages, this change will mainly affect new buyers who take out large mortgages. Before the new tax law, homeowners could deduct interest paid on a home equity loan or line, or credit of up to $100,000, regardless of how the funds were used.

Similarly, there's no deduction for re-fi interest you were planning on using to pay for college, take a vacation, or finally master the sport of curling. PE firms typically use “leverage,” or borrowing, to finance their purchases. They use the assets of the target companies as collateral, just like a prospective homeowner uses the value of the purchased home as collateral for a mortgage.

IRS Clarifies Home Equity Loan Tax Deductions Under New Law

For alternative minimum tax purposes, however, you could deduct the interest on these amounts only if the home equity loan proceeds were used to buy or improve your first or second residence. There are limits on the amount of home equity loan and lines of credit interest that can be deducted because the new tax law caps the total amount of home-related interest that can be written off. Interest on mortgage debt up to $750,000 can be deducted on homes purchased after Dec. 15, 2017.

For taxpayers itemizing deductions on their individual tax return, the mortgage interest deduction and the home equity interest deduction are both still a valuable component of your tax planning. For more information on the mortgage interest or home equity interest deduction, please contact Gloria McDonnell. Historically, borrowers could deduct home equity interest on loans up to $100,000 ($50,000 for married people filing separately).

Interest on Home Equity Loans Is Still Deductible, but With a Big Caveat

Before joining Bankrate in 2020, he wrote about real estate and the economy for the Palm Beach Post and the South Florida Business Journal. Casualty and theft losses – The itemized deduction for casualty and theft losses has been suspended except for losses incurred in a federally declared disaster. There is no longer any deduction for interest on home equity loans, regardless of when the debt was incurred. Note that in 2017 the exemption is subject to a phase-out that begins with adjusted gross incomes of $261,500 ($313,800 for married couples filing jointly). It phases out completely at $384,000 ($436,300 for married couples filing jointly). Failure-to-file and failure-to-pay.The IRS will consider any reason that establishes that you were unable to meet your federal tax obligations despite using “all ordinary business care and prudence” to do so.

TaxesFor most tax deductions, you need to keep receipts and documents for at least 3 years. The rules no longer allow you to use home equity loans to get tax-deductible financing for such things as consumer debt and tuition. You just can’t take the interest deduction on the amount used for those purposes, Ms. Weston said. That is because any acquired goodwill and other intangible assets may be written off over 15 years, even if these assets do not lose value.

However, because your $80,000 HELOC was taken out in 2018, the TCJA $750,000 limit on home acquisition debt apparently precludes any deductions for the HELOC interest. That’s because the entire $750,000 TCJA limit on home acquisition debt was absorbed by your grandfathered $800,000 first mortgage. So, the HELOC apparently must be treated as home equity debt, and interest on home equity debt can’t be treated as deductible qualified residence interest for 2018 through 2025. Under the old rules, taxpayers weren’t required to make a distinction between using home equity debt for home improvements vs. other uses — unless they were subject to the alternative minimum tax .

Also, you can refinance that existing mortgage and keep deducting the interest on up to $1 million of debt, so long as you don’t increase the amount you owe with the refi. The sweeping tax bill signed into law just before the 2017 holidays brings changes for virtually all homeowners -- but, for the most part, not until you file your 2018 tax return in 2019. All of this is subject to the new $750,000 debt limit on the total amount of all loans.

“Now the only people who can take this deduction are military service members moving for assignment,” Zimmelman said. President Donald Trump's tax plan eliminated several valuable deductions, but not all of them. TaxesWhat you can deduct, such as property tax, and what you can’t — but there are definitely more cans than can’ts. Providing reliable accounting, tax expertise and financial consulting services to individuals, businesses and not-for-profit organizations.

No comments:

Post a Comment